2 videos of aurora-borealis looking clouds before major earthquake in China. Very cool. Clearly there are things about geophysics that we don't understand yet.

http://www.youtube.com/watch?v=KKMTSDzU1Z4

http://www.youtube.com/watch?v=hzVamNQzfYA&feature=related

Tuesday, May 20, 2008

Wednesday, May 7, 2008

Oil, Oil, Everywhere

By Kevin Drum

May 7, 2008

"It's not that the genie is out of the bottle — it's that 100 genies are out of the bottle," said Daniel Yergin, chairman of Cambridge Energy Research Associates. Normally known for optimistic forecasts of lowering oil prices, Mr. Yergin's firm now says the price could rise to $150 a barrel this year.

The world's diminished spare production capacity remains the strongest single catalyst for high prices, Mr. Yergin says. The world's safety cushion — the amount of readily available oil that could be pumped in a moment of crisis — is now around two million barrels a day, according to most estimates. That's just 2.3% of daily demand, and nearly all of the safety cushion is in one country, Saudi Arabia. Everyone else is pretty much pumping all they can, which makes the world vulnerable to political or other shocks.

Saying Daniel Yergin is an optimist is like saying Chris Matthews is annoying. Yergin basically thinks peak oil is Luddite crankery and that new technology will allow us to continue increasing production for at least the next several decades. He's the Pollyanna of the oil patch.

Now, I'm sure he'd say that his current pessimism is based not on a fundamental reevaluation of recoverable reserves, but instead on "aboveground" issues: political instability, terrorism, lack of investment, and so forth. Still, if even Daniel Yergin thinks oil prices are headed upward, it's a pretty good guess that oil prices are headed upward.

Way interesting. Oil is well over $120/bbl as I write this. The nature of bull markets is that folks who've been bearish all along start throwing in the towel and getting on the bullish bandwagon late in the game. When you can't find a pessimist; it is a sign the bull market is getting old.

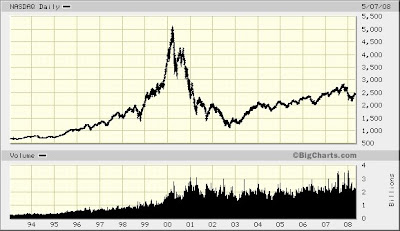

But, as a wise friend pointed out; the end of a bull market is where the most spectacular profits can be made. He pointed out some history on this, especially the NASDAQ tech bubble that happened a few years ago. Check out the chart below:

Half the NASDAQ bubble gains were made in the last four months of its bull market, roughly between November 1999 and March 2000. Prior to that; it built fairly steadily at a minor geometric pace since 1995. This shows up a bit more clearly on the log plot below:

Using the NASDAQ bubble as a basis to quantify estimates, could Yergin throwing in the towel be a sign we are going to have a "superspike" on oil prices that may double current prices? Possibly only lasting months and followed by a crash down to 25% or so of the peak price? The most amazing profits are made in the last legs of a bull. What separates the men from the boys is: who's got the guts to stick in to get to the peak and who's got the brains to time the sell at close to the peak?

Time will tell. If I really knew the answers to such a question I'd be rich! Sure gets my Spidey Sense tingling though.

May 7, 2008

OIL, OIL, EVERYWHERE....The price of oil closed at $122 today. But where's it going next? According to this AP dispatch, one analyst thinks it's likely headed up to $200 while another thinks it's probably headed down to $80. Yawn. This reaction, however, grabbed my attention:

"It's not that the genie is out of the bottle — it's that 100 genies are out of the bottle," said Daniel Yergin, chairman of Cambridge Energy Research Associates. Normally known for optimistic forecasts of lowering oil prices, Mr. Yergin's firm now says the price could rise to $150 a barrel this year.

The world's diminished spare production capacity remains the strongest single catalyst for high prices, Mr. Yergin says. The world's safety cushion — the amount of readily available oil that could be pumped in a moment of crisis — is now around two million barrels a day, according to most estimates. That's just 2.3% of daily demand, and nearly all of the safety cushion is in one country, Saudi Arabia. Everyone else is pretty much pumping all they can, which makes the world vulnerable to political or other shocks.

Saying Daniel Yergin is an optimist is like saying Chris Matthews is annoying. Yergin basically thinks peak oil is Luddite crankery and that new technology will allow us to continue increasing production for at least the next several decades. He's the Pollyanna of the oil patch.

Now, I'm sure he'd say that his current pessimism is based not on a fundamental reevaluation of recoverable reserves, but instead on "aboveground" issues: political instability, terrorism, lack of investment, and so forth. Still, if even Daniel Yergin thinks oil prices are headed upward, it's a pretty good guess that oil prices are headed upward.

Way interesting. Oil is well over $120/bbl as I write this. The nature of bull markets is that folks who've been bearish all along start throwing in the towel and getting on the bullish bandwagon late in the game. When you can't find a pessimist; it is a sign the bull market is getting old.

But, as a wise friend pointed out; the end of a bull market is where the most spectacular profits can be made. He pointed out some history on this, especially the NASDAQ tech bubble that happened a few years ago. Check out the chart below:

Half the NASDAQ bubble gains were made in the last four months of its bull market, roughly between November 1999 and March 2000. Prior to that; it built fairly steadily at a minor geometric pace since 1995. This shows up a bit more clearly on the log plot below:

Using the NASDAQ bubble as a basis to quantify estimates, could Yergin throwing in the towel be a sign we are going to have a "superspike" on oil prices that may double current prices? Possibly only lasting months and followed by a crash down to 25% or so of the peak price? The most amazing profits are made in the last legs of a bull. What separates the men from the boys is: who's got the guts to stick in to get to the peak and who's got the brains to time the sell at close to the peak?

Time will tell. If I really knew the answers to such a question I'd be rich! Sure gets my Spidey Sense tingling though.

Saturday, May 3, 2008

Oil Price May Go Up to $250, Warn Experts

Syed Rashid Husain

Crude prices continue to baffle analysts and pundits. With the $100-era a well established fact in our daily life, there is now a growing chatter within the energy fraternity that $200 a barrel may not be a far fetched idea altogether. Is another global oil shock now gathering pace?

With limited additional supplies, alternative fuel still some decades away and demand far from collapsing, Deutsche Bank is pointing to a “huge risk” that oil prices would continue to rise in the near to mid-term.

“There is a huge risk that the oil price simply continues to escalate until it gets to some level (possibly $250) when demand finally collapses because ordinary people can no longer afford to burn as much energy as they are burning now,” Adam Sieminski, Deutsche Bank’s chief energy economist, wrote in a report last Friday.

Pointing to the reasons behind the analysis, Sieminski underlines, “Oil supply growth in non-OPEC countries is struggling at a time when OPEC has been cautious with its production policies.”

In order to analyze the situation further, we need to look at historical facts too. In the early 1980s, oil demand collapsed only after nominal oil prices rose by a factor of 10 between 1970 to 1973 and 1980 to 1983, from about $3.50 a barrel to $35. Based on the empirical example of factor of 10, Sieminski deduces that since oil averaged about $25 a barrel from 2000 to 2003, prices would have to increase to $250 a barrel in 2010 to 2013 to have the same effect on oil users this time around.

Sieminski continues to argue that strengthening of the dollar would take time to stem the flow of investment into commodities, and alternative energies, such as solar power or biofuels, are at least a decade away from contributing to energy supply.

A Bloomberg report also quoted information provider Global Insight as projecting that crude oil could peak in the US at $135 a barrel in the next two months. Oil might rise to $135 as the declining dollar draws investors seeking a currency hedge, before new supplies see prices fall, Global Insight’s Simon Wardell was quoted as saying.

And in the meantime, OPEC president Chekib Khelil too has joined the chorus, hinting at significantly firmer crude markets in the near term. Projecting that oil prices could even hit $200 a barrel, Khelil blamed weakness in the dollar and global political insecurity for the current market woes. Establishing a direct relationship between the sinking dollar and the ascending crude prices, Khelil claimed that with the dollar losing one percent of its value, oil prices rise by $4 a barrel and vice versa.

Talking to Algeria’s El Moudjahid newspaper he argued, “I don’t think that any increase in production could help lower (crude) prices, because there is a balance between supply and demand and the stocks of gasoline in the United States have recorded a surplus and are at their highest level for five years.”

And OPEC has a point. Energy futures fell sharply last Wednesday after surprising jump in the US crude oil and distillate fuel inventories last week. In its weekly inventory report, the US Energy Department’s Energy Information Administration said crude oil inventories rose by 3.8 million barrels, more than double the increase that analysts surveyed by energy research firm Platts had expected.

Meanwhile, inventories of distillates, which include heating oil and diesel fuel, rose by 1.1 million barrels, more than seven times the expected increase.

Some analysts now believe record gas prices are depressing demand for gasoline. “The demand just isn’t there, and there’s plenty of supply,” admits Phil Flynn of Alaron Trading Corp. in Chicago.

On the other hand, despite the official OPEC insistence on not raising the output any further, most Gulf Arab states have been producing at higher levels recently. As per the Joint Oil Data Initiative (JODI), compiled by the Riyadh based International Energy Forum, Saudi Arabia lifted its rude oil supply in January and February to one of its highest levels in many years, while the UAE, Kuwait and Iran also pumped at near capacity. Qatar, a relatively smaller oil producer but a major gas power, also boosted its crude output to record levels in February.

Saudi Arabia’s output climbed to 9.216 million barrels per day (bpd) in February and an average of 9.205 million bpd in January and December. The February level was the Kingdom’s highest production in more than two years and one of the highest in a decade. And despite this high output over the last few months, Saudi Arabia maintained a spare capacity of 1-1.5 million bpd - as per its commitment as a responsible oil producer. Indeed being at the top position also brings in a number of responsibilities too. And Saudi Arabia seems fully aware of it.

Although March figures were not available yet, independent estimates showed Saudi and the Gulf output remaining almost at the February levels, if not higher.

The UAE also pumped 2.716 million bpd in February, up from around 2.700 million bpd in January. The output is close to the country’s sustainable output capacity and is the highest since the Emirates began commercial crude exports in the early 1960s.

Kuwait said it boosted its production, including output from the Neutral Zone, which it shares with Saudi Arabia, by nearly 200,000 bpd to a record high of 2.797 million bpd in February. Iran also pumped at maximum capacity of around 4.120 million bpd while Qatar raised production to its highest ever level of 862,000 bpd in February.

And the above figures once again brings under focus that the real issue afflicting the crude markets is not the output factor, as claimed by some in the industrialized world. Output may be one of the many important factors but indeed not the main factor. Other factors, much beyond the control of the OPEC seem to be equally responsible for the woes of the market, if not more, one has to concede.

Lower oil production is the real story

By LOREN STEFFY

Copyright 2008 Houston Chronicle

Copyright 2008 Houston Chronicle

Eleven billion dollars is not enough.

That, at first blush, seemed to explain how Exxon Mobil Corp. could earn that much money in three months and still see its stock fall 4 percent.

Wall Street expected more, and so did Exxon Mobil investors. At a time of record oil prices, America's biggest oil company reported an earnings increase that was the smallest among its peers.

The profit is what captures everyone's attention, but there's a bigger concern hidden amid the numbers of Exxon Mobil's earnings.

The company's worldwide oil production fell 10 percent, to just under 2.5 million barrels a day.

Some of the decline came from Exxon Mobil's dispute over the seizure of assets by the Venezuelan government, but even excluding those assets, the company's production declined. Overall production, including natural gas, fell 3 percent.

While Exxon Mobil boosted production from fields in West Africa and the North Sea, the gains weren't enough to offset declines from aging oil fields, the company said.

The company blamed the decline in part on its contracts with oil-producing countries, which allow those countries to claim a larger share of oil volumes as prices rise. In other words, the higher prices go, the less oil Exxon Mobil gets.

As those countries benefit from higher prices, living standards rise and, as I mentioned last week, their own demand for oil increases. That, in turn, means less oil for companies such as Exxon Mobil over the long term.

The problem isn't unique to Exxon Mobil.

Other major oil companies also offered a stark production picture. BP's was unchanged from a year earlier. Shell reported a gain only because it boosted natural gas production, which offset lower oil output. ConocoPhillips reported an increase but attributed it to its 20 percent stake in Russia's Lukoil.

With national oil companies now holding most of the world's reserves, companies like Exxon Mobil are left with few places to look for new production.

The public, though, has little concern for Exxon Mobil's travails. We only care about what we see from our side of the pump, and that means the price and the profits of the company whose name is atop the sign.

Exxon Mobil has reported earnings between $9 billion and $11 billion in almost every quarter since late 2005, and every time it does, the public outcry grows.

Capitalizing on outrage

Politicians are quick to capitalize on that outrage.

"I believe we should impose a windfall profits tax on big oil companies and use that money to suspend the gas tax and give families relief at the pump," Hillary Clinton said in a statement addressing Exxon Mobil's earnings. A typical family, she claims, would save $70. John McCain already has called for a "gas tax holiday."

A closer reading of Exxon Mobil's earnings statement, though, shows Clinton is missing the point.

Her plan, and McCain's, would essentially lower gasoline prices at the pump. And how will we respond? We'll drive more. We're talking about summer, after all. Time to load up the kids in the land yacht and cruise to Destin at 12 miles to the gallon.

As demand rises, it depletes supply even further, and that, in turn, drives prices up in the world market. Shortages aren't solved by using more.

Barack Obama, by the way, has proposed a broader windfall profits tax on the industry based on crude prices, which the companies don't control. He'd tax oil over $80 a barrel, Bloomberg News reported, even though futures markets are indicating oil will stay above $100 through 2016.

Using this logic, we should tax pizza places because of soaring cheese prices.

They don't like it either

As I've said before, oil companies don't welcome the numbers we're now seeing at the pump. Not only do they cut into refining margins — another reason Exxon Mobil's profit didn't grow as much as expected — they make us start buying Priuses in spite of their bean-pod appearance.

So the public and politicians decry Exxon Mobil's profit while the market frets over a mere 17 percent increase. Both miss the more disturbing numbers, the ones that portend greater problems, not just for the oil companies but for all of us who use their products.

It's not a question of whether $11 billion is too much or not enough. It's a question of whether 2.5 million barrels is.

Loren Steffy is the Chronicle's business columnist. His commentary appears Sundays, Wednesdays and Fridays. Contact him at loren.steffy@chron.com. His blog is at http://blogs.chron.com/lorensteffy/.

The Peak Oil Crisis: The Half-Life For Air Travel

Written by Tom Whipple

Thursday, 01 May 2008

In recent weeks, airlines around the world have been reporting substantial losses, declaring bankruptcy or completely shutting down. So far the losses have been mostly of small airlines, but many of the large ones have started to thrash around for merger partners. At $3.71 a gallon, jet fuel is now the single largest expense an airline faces.

In 2000, the airlines fuel bill was $14 billion. It is now pushing $60 billion and climbing. Southwest, the most profitable carrier, recently announced that this year’s fuel bill will be $500 million more than last year and equal to 2007 profits. During the first quarter of 2008 American airlines lost $328 million; Delta lost $274 million; United lost $537 million; Continental $80 million; Northwest $191 million; and US Airways $236 million. Only Southwest Airlines, which did a better job of hedging its fuel than the others, made a profit.

It is clear we are going to see major changes in air travel shortly.

For some time now, airlines have been eliminating frills, raising prices, filling the planes and effecting whatever other economies come to mind. After the summer flying season ends next September, many airlines are planning to retire 5-10 percent of their least efficient aircraft, thereby reducing their flight schedules by a similar amount.

Knowledgeable observers are expressing doubts these moves will be enough. People are starting to talk about $200 oil which implies that airline fuel costs will double again. Newer aircraft are more efficient, but the improvements are nowhere near what is necessary to keep up with surging fuel costs and, as Continental Airlines concluded this week, there is not enough financial benefit in a merger to keep up with costs.

Airlines are continuing to raise fares -- the average ticket is up 10 percent over last year -- but at some price point the airlines will drive away discretionary travel and they will be left with only essential business and personal travel that is unlikely to fill many planes. On top of the fuel prices is the current economic downturn which is likely to start impacting discretionary travel before the year is out. In short, airplanes simply can’t make money while charging affordable fares at current, much less prospective, fuel prices. The era of 500 mph travel for most people is nearly over.

There is no obvious way out of this dilemma unless there is a major breakthrough in the efficiency of aircraft. Fares will continue to rise. Flights will be cut. Smaller cities will lose their air service. Shorter trips will be eliminated as being too expensive. More seats are likely to be squeezed on planes and one manufacturer is even pondering seat-less planes in which passengers are strapped to boards during the flight.

Ten or 15 years from now, air travel is likely to be significantly reduced; will be patronized by business travelers or the very wealthy; and will be limited to trans-oceanic or long-distance flights between major population centers.

Consolidation of the major airlines and the demise of the smaller regional carriers has already started. After a number of rounds of consolidation, we will be down to only a handful of national or multi-national airlines probably subsidized by governments on “national security” grounds.

While the demise of inexpensive discretionary air travel has ramifications for many industries, in the first instance tourism is likely to be hit the hardest.

Ignoring for the minute the likely effects of $4 or $5 gasoline in California this summer, Las Vegas reports that nearly half of its tourists arrive by air. To make matters worse, resort operators have recently spent billions upgrading their facilities to the $300 a night places that are less likely to attract drive up customers. The same pattern can be repeated at air-dependent tourist attractions all over the world.

There is still a remarkable amount of denial in the airline business. This week Airbus released a forecast showing that the number of large commercial aircraft will grow from 15,000 to 33,000 in the next 20 years and that the number of passengers will triple.

If there is to be a long-term future for air travel, it is unlikely to be with liquid fuel powered turbines driving heavier than air devices. The U.S. Air Force is currently embarked on a campaign to convince the Congress to buy it a multi-billion dollar facility to convert coal to jet fuel and a couple of airlines are busy demonstrating that their planes will run on biofuels.

While limited use of coal to liquid fuel or biofuels for aircraft may see limited use, neither of these replacements is likely to produce enough affordable fuel to keep Airbus’s 33,000 large transport jets in the air 20 years from now.

Over the longer run, the development of hydrogen powered aircraft might prove feasible or perhaps lighter-than-air dirigibles might be developed to the point where they can move people and goods efficiently over long distances. In any case, the day of the ubiquitous kerosene-powered jet transport which revolutionized travel for many of us in the second half of the 20th century is likely to be shorter than most realize.

Friday, May 2, 2008

Food crisis looms for Japan as prices rise

By Julian Ryall, in Tokyo

Last Updated: 1:04AM BST 02/05/2008

This is of particular note:

Last Updated: 1:04AM BST 02/05/2008

Japan is facing its first food shortages in almost 40 years, with supermarkets close to running short of stocks.Article continues

n the last month, the price of milk, soy sauce, bread, noodles, pasta and cooking oil have all risen as makers are forced to pass on rising costs.

Butter has already begun to disappear from supermarket shelves as surging global grain prices make it impossible for Japan's dairy farmers to increase milk production. Retailers warn that other goods could follow soon.

With the global food crisis beginning to bite in one of the world's most powerful economies, more than 80 per cent of Japanese said that increasing prices were having an impact on their household spending. Many shoppers said they were switching to cheaper brands or buying in greater bulk.

This is of particular note:

A major concern for Japan's government is that its farmers can produce only about 40 per cent of the food consumed each year by its 128 million inhabitants. This is the lowest proportion for any industrialised nation and also adds to transport costs, which have become a larger burden than elsewhere.

Subscribe to:

Posts (Atom)